11

11

Keywords: homeowners insurance USA 2026 · flood insurance · home insurance cost · best home insurance companies · wildfire coverage

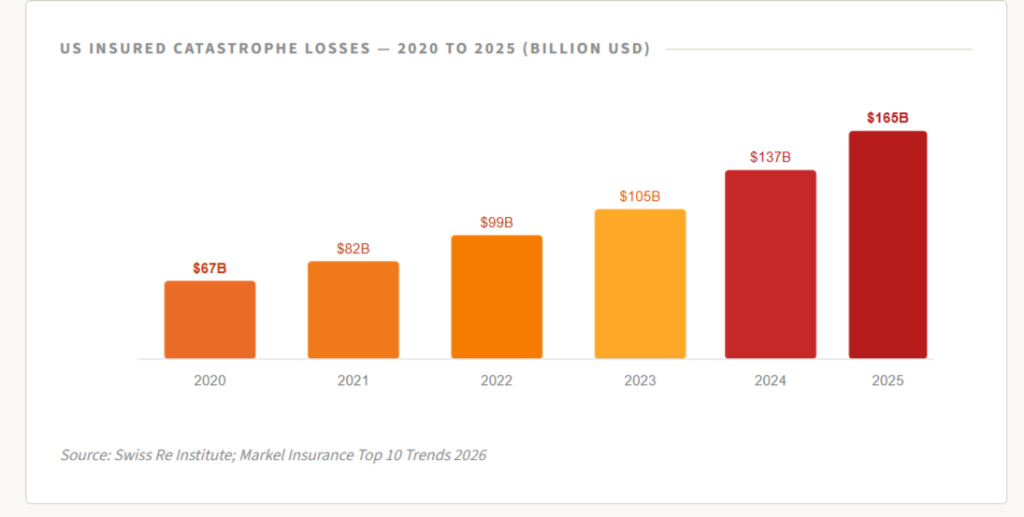

he Los Angeles wildfires of early 2025 caused an estimated $40 billion in insured losses. Hurricane Milton struck Florida in 2024 with $50 billion in damage. In 2026, climate-driven catastrophes are not distant risks — they are annual certainties. For American homeowners, the question is no longer whether a disaster will strike, but whether they are adequately covered when it does.

A standard HO-3 homeowners policy — the most common form — covers four major categories. Dwelling Coverage pays to rebuild your home’s structure if it’s damaged by covered perils like fire, lightning, windstorm, or vandalism. Personal Property replaces your belongings — furniture, electronics, clothing, appliances. Liability Coverage protects you if someone is injured on your property and sues you. Additional Living Expenses (ALE) pays for hotel bills and meals while your home is being repaired after a covered loss.

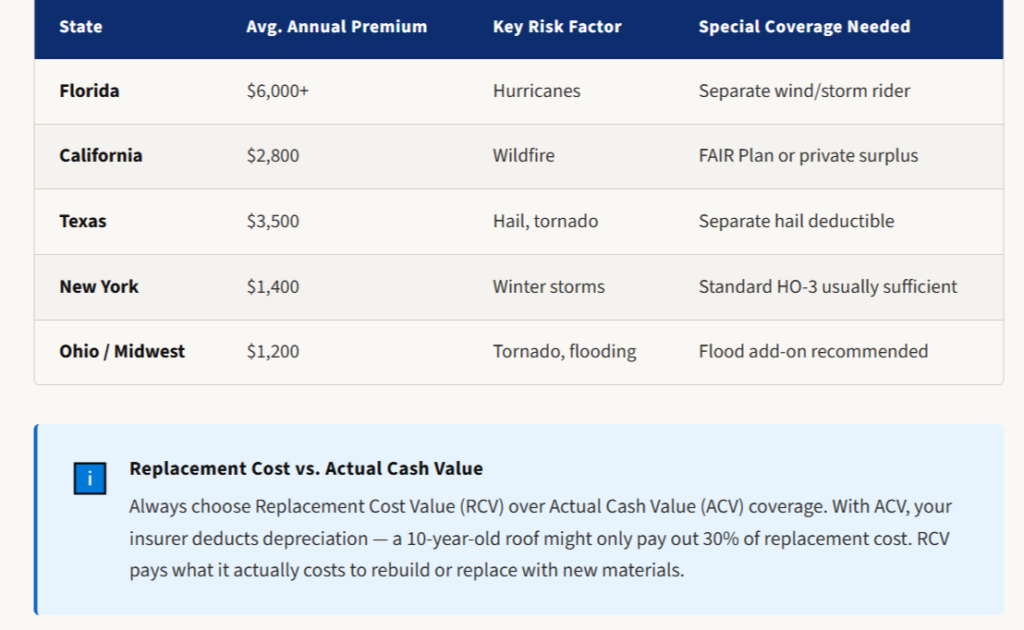

Standard homeowners policies explicitly exclude flood damage and earthquake damage. In 2026, these two gaps expose millions of American homeowners to uninsured losses. If you live in a FEMA-designated flood zone, you are typically required by your mortgage lender to purchase flood insurance through the National Flood Insurance Program (NFIP) or a private flood insurer. But even outside designated flood zones, 40% of flood claims come from properties in moderate-to-low risk areas. Earthquake insurance, sold separately by private carriers, is strongly advisable in California, the Pacific Northwest, and parts of the Midwest.

Compare quotes from State Farm, Amica, USAA, and Erie Insurance — consistently rated the best for claims satisfaction. Use Policygenius to compare multiple carriers at once. Don’t let under-insurance turn a disaster into a financial catastrophe.

Keywords & Hashtags

#HomeownersInsuranceUSA2026#FloodInsuranceUSA#EarthquakeInsurance#WildfireInsurance#BestHomeInsurance2026#NFIPFloodInsurance